Getting pre-approved for a mortgage is one of the most difficult processes in the home purchasing process. You won't know how much you'll be eligible to borrow or whether you can even buy a home until you receive that permission letter. But once you had that preapproval letter in your possession, you undoubtedly sighed with relief and began searching seriously.

Your borrowing status may swiftly alter in risky lending circumstances, such as during a crisis, a recession, or when the Federal Reserve is anticipated to hike rates. So how long is a pre-approval for a mortgage valid?

Continue reading to find out more about the pre-qualification and loan pre-approval processes, their importance, and, most crucially, their duration.

What is the Meaning of Mortgage Pre-Approval?

A pre-approval for a mortgage serves as a trial run for your real mortgage. Your financial position is taken into account throughout the pre-approval process to determine the amount of the loan and the interest rate you qualify for. Additionally, you'll get a projected housing payment each month, which is important for budgeting.

Pre-approvals provide purchasers the information they need to decide how much house they want to buy as well as the precise amount they are permitted to purchase.

What Is Pre-qualification for a Mortgage?

When a lender says you are pre-qualified, it indicates that they have received your financial information and have acknowledged its validity without doing any real verification. They haven't checked your credit, gotten in touch with your job, etc.

You won't get an actual loan amount from pre-qualification; instead, you'll get an estimate of how much you may be able to borrow. Although having pre-qualification is good, pre-approval will ultimately be required. But it is better to wait for approval than to look for a quick loan with the request "need money now" and then pay high interest.

What Is a Mortgage Preapproval Letter?

The process of purchasing a property may be significantly aided by a letter of pre-approval. It demonstrates to sellers that you are serious about purchasing a house and that you can probably count on a mortgage lender to approve you for a loan promptly.

Although it's not exactly a promise, a preapproval letter from a lender indicates that it is prepared to offer you a certain amount of money for a mortgage.

Your credit history, income, and assets will all be examined by the lender to establish how much you are eligible for. The letter will then include that figure and maybe some conditions for receiving the loan, such as keeping your job or refraining from taking on any new debt.

You may narrow your search for houses to your price range with the aid of a preapproval letter. This is crucial in markets with intense competition since you won't want to spend time looking at houses that are too expensive. Many sellers need a preapproval letter before accepting an offer since it might show them that you are a serious buyer.

Why a Mortgage Pre-Approval Is Necessary?

A letter of pre-approval is still a crucial step in the home-buying process even if it does not ensure that your formal loan application will be granted.

A letter of pre-approval not only outlines the price range of properties you should search for but also gives you access to additional sellers who are interested in working with serious buyers.

By demonstrating that you have permission to spend up to a certain amount but no more, a letter of pre-approval may even enable you to negotiate a better bargain.

You will need a letter of pre-approval to be taken into consideration if the seller has cash purchasers putting compelling bids on the house you're interested in but you can't pay with cash.

What Distinguishes Pre-Approval From Pre-Qualification?

In fact, pre-approval and pre-qualification are quite different concepts. Pre-qualification only provides you with an approximate sense of your borrowing capacity and ability to qualify for a home loan. Pre-qualification is only based on verbal information; there is no paperwork or credit check. As a result, it is less trustworthy and does not represent a funding guarantee. You won't have as much influence with sellers if you just have a pre-qualification letter.

Don't panic if you have been pre-approved but your letter's window has passed due to shopping. Simply request another, and you'll be back out there quickly looking at additional houses.

How Long Do Pre-Approvals For Mortgages Last?

Pre-approvals for mortgages normally last for 90 days. Your financial status may vary over time, interest rates are always fluctuating, and credit ratings are updated regularly. Your maximum purchase price may be impacted by all of these factors, for better or worse.

When the 90-day timeframe is approaching and you still haven't located a property, get in touch with your mortgage advisor and let them know you'd want to have your pre-approval updated. You'll provide some new supporting papers, and they'll update your credit report and go through everything once more.

How Many Letters of Preapproval Should You Receive?

Multiple preapproval letters are possible, but they may damage your credit. A hard inquiry is made on your credit report because lenders analyze your credit to write a letter. A hard query may lower your credit score by many points, and lenders may be wary of you if you make too many inquiries.

But there is a grace period. It will only appear as one hard credit draw on your credit report if you apply for preapproval with different mortgage lenders in a period of 14 days or less. Therefore, avoid waiting many weeks between applications while you're shopping.

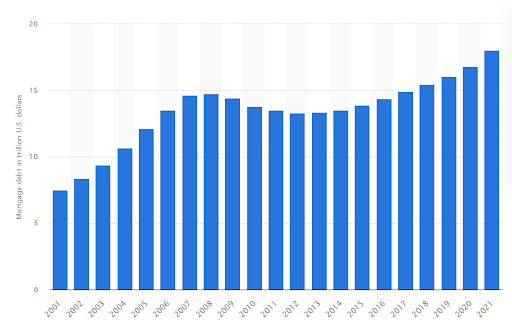

The overall amount of mortgage debt in the United States has increased recently, despite a brief period of decline after the collapse of the U.S. housing bubble and the global financial crisis. Mortgage debt increased from 16.8 trillion dollars in 2020 to 18 trillion dollars in 2021. People are increasingly in need of housing and this is a fairly competitive market. To increase your chances of success with your mortgage plan, you'd better get pre-approval.

Conclusion

Lenders look at five things during a mortgage pre-approval to make sure customers will be able to repay their loan. To be pre-approved, prospective borrowers fill out a mortgage application and submit the necessary paperwork, including proof of assets, evidence of income, a credit report, and job verification.

Borrowers should often wait to be preapproved until they're prepared to actively look for a property. By doing this, they may be sure that their preapproval letter won't expire and can safely place a bid on the house they want to buy.

Now you know all the basic things about mortgage pre-approval and we hope it will help you in buying your dream home.

Other Articles Related to Your Search

How to Choose the Right Mortgage for your Life Goals

(0) comments

We welcome your comments

Log In

Post a comment as Guest

Keep it Clean. Please avoid obscene, vulgar, lewd, racist or sexually-oriented language.

PLEASE TURN OFF YOUR CAPS LOCK.

Don't Threaten. Threats of harming another person will not be tolerated.

Be Truthful. Don't knowingly lie about anyone or anything.

Be Nice. No racism, sexism or any sort of -ism that is degrading to another person.

Be Proactive. Use the 'Report' link on each comment to let us know of abusive posts.

Share with Us. We'd love to hear eyewitness accounts, the history behind an article.