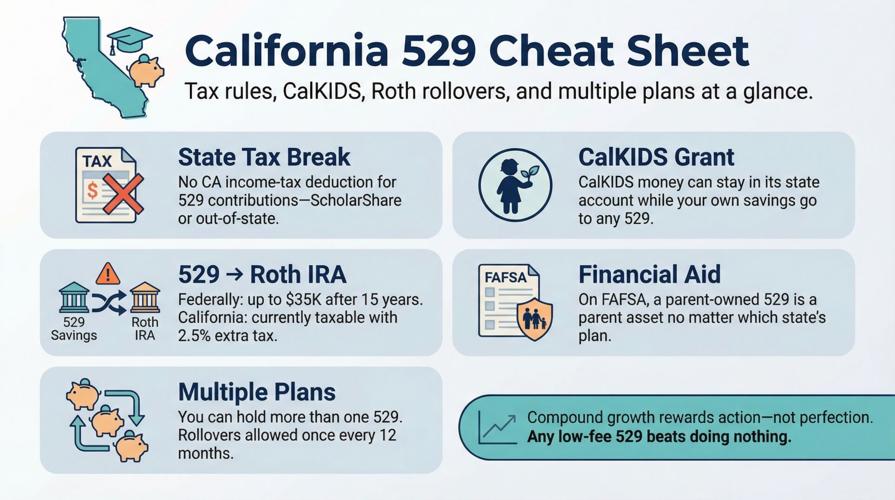

California hands you a quirky deal on college savings: your 529 grows tax-free, yet you get zero state income-tax break when you contribute (SavingforCollege). That hitch frees you to shop the entire country for a cheaper, better plan.

In this guide, we sift recent fee studies, Morningstar’s 2025 medals, and fresh plan updates to spotlight six programs that stretch every tuition dollar. You’ll see how each trims expenses, what investments it offers, and how a smart switch could add thousands to your child’s future balance.

First, we outline our scoring playbook. Next, we count down the winners—backed by a quick reference table—and tackle FAQs on CalKIDS grants, the new 529-to-Roth rollover, and juggling multiple accounts.

Ready? Let’s turn California’s “no-deduction” snag into a wide-open advantage and land the plan that fits you best.

How we picked the winners

We approached this search the way you would tackle a six-figure tuition bill: with sharp focus on cost and quality.

First, we gathered fresh fee sheets and performance data for every direct-sold 529 plan nationwide. Any program still quoting 2022 numbers went to the sideline. We zeroed in on plans that keep at least one core portfolio at or below a 0.25 percent all-in expense ratio, leaving you more money for textbooks instead of fund managers.

Next, we checked each contender’s independent grade. Morningstar’s 2025 medal list and SavingforCollege’s five-cap scores showed whether a plan’s process, oversight, and long-term results inspire outside confidence. Gold or Silver medals cleared the bar; anything lower raised a flag.

Cost was still king, so we weighted it heavily—40 percent of the final score. Independent ratings, menu flexibility, recent stewardship moves, ease of use, and capital-preservation choices filled in the rest. That blend let a plan like Illinois Bright Start, with its seventh Gold rating and 0.10 percent fees, claim the top spot, noted The Silicon Review.

We also rewarded continual fee trims. Utah’s my529 cut its administrative asset fee again in 2024, pushing most portfolios near 0.12 percent total cost, according to my529’s announcement. Momentum like that signals a culture of passing savings back to families.

Finally, we checked every feature from minimum opening deposits to gifting portals. If a plan demanded a hefty first check or buried investors in maintenance fees, we cut it. The result is a ranked short-list of six programs that combine microscopic expenses, transparent management, and friction-free onboarding. They are the clear standouts for Californians who are not locked into ScholarShare, and they are up next.

1. Illinois Bright Start 529 College Savings Plan

Bright Start tops our list for one reason: it lets your dollars sprint, not slog.

Illinois Bright Start 529 College Savings Plan official website screenshot

Its core index portfolios cost about 0.10 to 0.15 percent a year, pennies on every hundred you invest. Morningstar gave the plan its seventh Gold rating in 2025. Over an 18-year runway, a 0.15-point fee gap can leave an extra four-figure cushion for tuition, and if you’re weighing that benefit against alternatives like Roth IRAs or a plain savings account, Bright Start’s Comparing ways to save for college chart lines up the taxes, contribution limits, and financial-aid impact so the 529 advantage is crystal-clear.

The investment menu feels like a well-stocked farmers market. Choose a ready-made age-based track and be done in sixty seconds, or mix funds from eleven managers—Vanguard, Dimensional, T. Rowe Price, Dodge & Cox—for a custom recipe. Few 529s offer that breadth without piling on cost.

Ease matters, too. Opening an account takes a 25-dollar transfer and five minutes online. The dashboard is clean, the gifting link is share-ready before you finish your latte, and customer support answers quickly. Because Illinois offers the same features to all account holders, Californians get the full menu with no strings attached.

Bottom line: if you want tiny fees, deep fund choice, and a decade-long Gold track record in one package, Bright Start is your front-runner.

2. Utah my529

Utah’s plan is a long-time favorite for good reason: it cuts the fluff and gives you full control.

Utah my529 official 529 college savings plan website screenshot

Start with the cost. In August 2024, my529 trimmed its administrative fee by another basis point, pushing most age-based portfolios to roughly 0.12 percent all-in. That sits near the floor for any 529, letting more of your money compound instead of leaking away.

Flexibility is the next hook. Prefer autopilot? Pick one of four age-based tracks and let the glide path handle rebalancing. Want to engineer your own mix? The platform lets you dial allocations to a single percentage point across Vanguard or Dimensional funds. Few 529s reward both the set-it-and-forget-it saver and the hands-on tinkerer equally.

Ease of entry matters, too. There is no minimum to open; you can drop in ten dollars today and schedule the rest next payday. The interface feels modern, and Utah’s gift-link tool makes birthday contributions painless for grandparents who avoid paperwork.

Together, my529 delivers rock-bottom fees, elite customization, and a customer-first track record. For Californians who want maximum leeway without sacrificing returns, it is a strong second choice.

3. Massachusetts U.Fund College Investing Plan

Think of the U.Fund as the 529 that sits beside your Fidelity brokerage and works quietly for decades.

Massachusetts U.Fund College Investing Plan on Fidelity website screenshot

Fees come first. The plan’s index enrollment-year portfolios hover around 0.13 percent all-in, squarely in the ultralow camp. That small price tag is baked into Fidelity’s own index funds, so you do not pay another program layer on top.

Quality supports the bargain. Morningstar awarded the U.Fund a Gold rating for 2025, noting cleaner glide paths and steady fee cuts. In practice, the plan tracks market benchmarks almost tick for tick, letting compound growth do the heavy lifting.

Convenience seals the deal. Open an account in minutes with as little as fifty dollars, then view it alongside every other Fidelity holding on one dashboard. Automatic deposits, fractional investing, and a 2 percent cash-back credit card that sweeps rewards into the 529 all live under the same login. If you already trust Fidelity with your IRA or taxable account, adding a college bucket feels natural.

Investment choice stays streamlined rather than overwhelming. You get enrollment-year options for autopilot savers, a handful of risk-based static mixes, and individual index-fund portfolios for purists. No exotic fund families, no overwhelming menu; just a tight, low-cost lineup that covers global stocks and bonds.

For Californians who crave simplicity, top-tier ratings, and a familiar interface, Massachusetts offers a “set it and smile” solution that keeps both expenses and effort low.

4. Ohio CollegeAdvantage 529 Savings Plan

If Utah offers Lego-level customization, Ohio hands you an entire hardware aisle.

Pricing comes first. Index age-based portfolios sit near 0.15 percent in total annual cost, and even the priciest specialty funds stay under the half-percent line, keeping Ohio comfortably below California’s ScholarShare on a like-for-like check, according to the CollegeAdvantage fee table.

Breadth is Ohio’s signature. You can park cash in an FDIC-insured savings option or lock a slice into bank CDs. Prefer a pure Vanguard equity diet? It is there. Want Dimensional funds or a stable-value option that shields principal during junior-year jitters? Also there. Few 529s give you this many levers without forcing a future rollover.

Opening hurdles are low: twenty-five dollars gets you in, and the online portal makes juggling multiple kids’ accounts painless. CollegeAdvantage also runs seasonal promos that drop a small bonus into new accounts, a welcome perk for families who enjoy free money.

All told, Ohio is a Swiss Army knife of low-cost 529s: agile enough for DIY investors, safe enough for conservative savers, and cheap enough to stay in the running with our top three picks. If you value versatility as much as raw expense ratios, CollegeAdvantage deserves a hard look.

5. New York’s 529 Direct Plan

Sometimes the smartest move is the simplest one, and New York’s plan proves it.

New York’s 529 Direct Plan official website screenshot

Every portfolio uses Vanguard index funds, so expenses stay tiny at a flat 0.12 percent. Choose an enrollment-year option and the glide path shifts automatically from stocks to bonds as college nears. No tinkering, no second-guessing, just near-wholesale market returns.

Simplicity carries into signup. There is no minimum to open, and the website guides you from “start” to “funded” in under ten minutes. A pared-down menu means you spend time saving, not debating between look-alike choices.

Scale helps, too. As assets ballooned early, fees trended down while performance, powered by pure indexing, tracked benchmarks closely. Morningstar upgraded the plan to a Silver rating in 2023, noting disciplined oversight without extra complexity.

If you want a 529 that hums quietly in the background—letting you focus on SAT flashcards instead of fund lineups—New York offers one of the cleanest, cheapest paths available.

6. Pennsylvania 529 Investment Plan

Pennsylvania proves a plan can be both quiet and top tier.

Start with the numbers. After a string of fee trims, its index portfolios sit in the 0.18 to 0.21 percent range—just a hair above Utah and Illinois, and well below the national average, according to the PA 529 disclosure statement. Over an 18-year saving window, that tiny spread compounds into real money.

Low cost is only part of the draw. The menu blends simplicity with useful choices. Age-based tracks suit hands-off savers, while static mixes let you lock in a risk level you trust. Need true safety senior year? A built-in stable-value portfolio preserves principal without moving cash outside the 529.

Pennsylvania also skips hurdles. There is no minimum to open, making it easy to launch an account for every child—or grandchild—early. The dashboard mirrors New York’s clean interface, so first-time investors can automate contributions and move on with their day.

Morningstar’s analysts upgraded the plan to Gold in 2023 and reaffirmed that rating in 2025, citing steady fee pressure and performance that tracks the market closely.

For California families who want Vanguard-level expenses plus a few thoughtful extras, Pennsylvania delivers quietly and effectively.

At-a-glance: how the six plans stack up

Plan | Core index fee | Morningstar 2025 medal | Minimum to open | Standout feature |

Illinois Bright Start | ~0.10 % | Gold | $25 | Broad fund lineup plus seventh Gold rating |

Utah my529 | ~0.12 % | Gold | $0 | DIY custom portfolios down to 1 % slices |

Massachusetts U.Fund | ~0.13 % | Gold | $50 (or $15 via payroll) | Smooth Fidelity integration and 2 % cash-back card |

Ohio CollegeAdvantage | ~0.15 % | Silver | $25 | Mix of Vanguard, DFA, CDs, and stable-value option |

New York Direct | 0.12 % | Silver | $0 | Pure Vanguard indexing at the lowest sticker price |

Pennsylvania 529 | ~0.18 % | Gold | $0 | Gold-rated value plus built-in stable-value option |

Read the table as a menu, not a scoreboard. All six deliver bargain-level costs, strong oversight, and user-friendly features. Your choice simply depends on which extra—customization, brokerage convenience, or a cash option—matters most to you.

California-specific FAQs

Do I give up any tax break by leaving ScholarShare?

No. California offers no state income-tax deduction for 529 contributions, whether you fund ScholarShare or an out-of-state plan. Qualified withdrawals remain tax-free, so you can shop purely on fees and features.

What about CalKIDS money—does that force me to use ScholarShare?

CalKIDS deposits sit in a small state-owned account under your child’s name. You can let that grant grow there, while directing your own savings to any 529 you prefer. At withdrawal, you simply draw from both accounts.

Can I roll unused 529 dollars into a Roth IRA?

Federally, yes—up to 35,000 dollars after the 529 has been open 15 years. Today California treats that rollover as taxable income with a 2.5 percent additional tax, according to the Franchise Tax Board’s March 2025 update. Lawmakers are considering conformity, so watch Sacramento for updates.

Does picking, say, Utah over Illinois change my child’s financial-aid picture?

No. On the FAFSA, a parent-owned 529 is a parent asset regardless of the sponsoring state, and qualified withdrawals do not count as student income.

Can I hold more than one 529?

Yes. Many families keep a small ScholarShare account for CalKIDS money and a larger balance in a low-cost out-of-state plan. You may also roll assets from one plan to another once every 12 months if a different option later proves better.

How fast should I decide?

Compound growth rewards action, not perfection. Any of the six plans above beats doing nothing and almost certainly outruns a higher-fee alternative. Open the account that feels easiest today; you can adjust later if needed.

(0) comments

We welcome your comments

Log In

Post a comment as Guest

Keep it Clean. Please avoid obscene, vulgar, lewd, racist or sexually-oriented language.

PLEASE TURN OFF YOUR CAPS LOCK.

Don't Threaten. Threats of harming another person will not be tolerated.

Be Truthful. Don't knowingly lie about anyone or anything.

Be Nice. No racism, sexism or any sort of -ism that is degrading to another person.

Be Proactive. Use the 'Report' link on each comment to let us know of abusive posts.

Share with Us. We'd love to hear eyewitness accounts, the history behind an article.